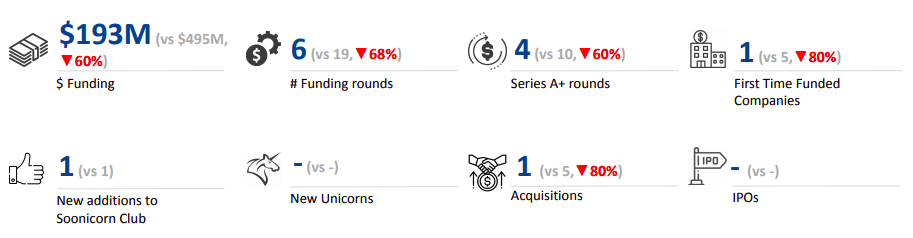

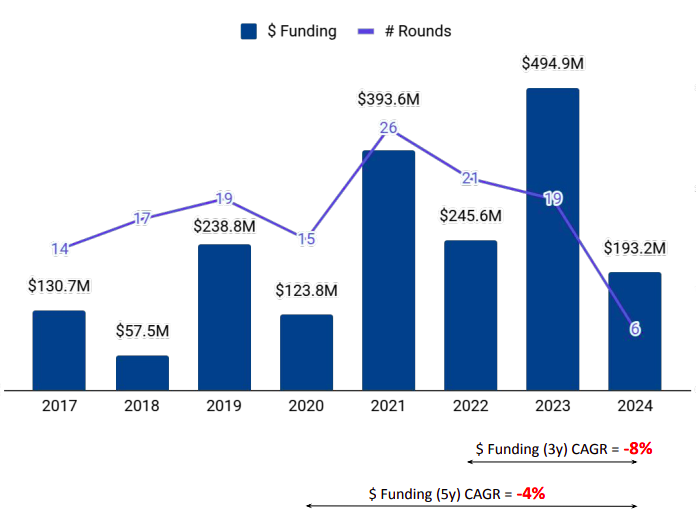

The Southeast Asia (SEA) InsurTech market has experienced significant fluctuations in funding over the past two years. The sector saw its highest-ever funding in 2023, with a total of $495 million raised. However, 2024 marked a sharp decline, with only $193 million secured—a staggering 61% drop compared to the previous year (2023). This trend aligns with a global funding downturn across sectors, driven by macroeconomic uncertainties, higher inflation, and increased interest rates, creating a more cautious investment landscape.

Beyond financial market challenges, geopolitical factors have added complexity for Southeast Asian nations. Despite these challenges, the region has demonstrated growth and economic adaptability in recent years.

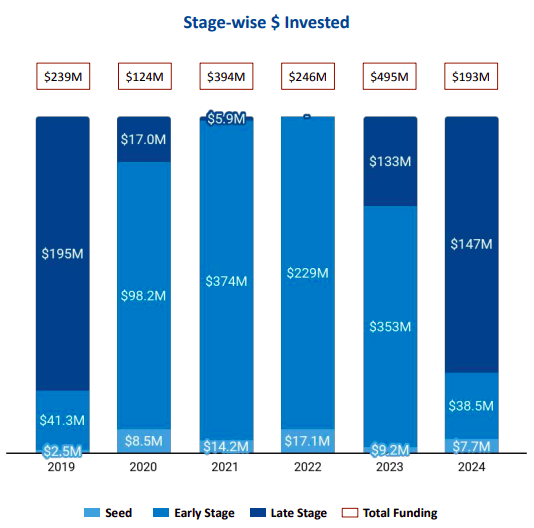

The SEA InsurTech sector’s total funding of $193 million in 2024 represents a sharp 61% decline compared with $495 million in 2023 and a 21% drop from $245.6 million in 2022.

Seed-stage funding fell 16% to $7.7 million in 2024 from $9.2 million in 2023, while early-stage investments plummeted over 80% to $38.5 million in 2024 from $353 million in 2023. Late-stage funding witnessed an 11% uptick to $147 million in 2024, compared with $133 million in 2023.

Q4 2024 saw the maximum investment activity across all quarters, with $105 million raised, accounting for nearly half of the total funding for the year. Further, the second half (H2) of 2024 emerged as the most active funding period, raising $111 million—a 35% increase from H1 2024 ($82 million) but a 50% decline from H2 2023 ($231 million).

Singapore has solidified its position as a global hub for tech startups, ranking as the fourth highest-funded country in FinTech investments in 2024, following the US, UK, and India. Meanwhile, Indonesia and Vietnam are experiencing significant expansion in the manufacturing sector. Leading global companies have established new manufacturing units in these countries, attracted by competitive labour costs and favourable foreign direct investment (FDI) policies. These opportunities, coupled with increasing government support, are expected to accelerate economic growth in the region.

The sector saw just one $100M+ funding round in 2024, as against two in the previous year. Bolttech, a provider of insurance-as-a-service solutions, raised $100 million in its Series C funding round, becoming the largest round of the year.

Insurance IT, Internet-First Insurance Platforms, and Employer Insurance attracted the highest funding in SEA’s InsurTech sector. Insurance IT companies secured funding worth $135 million in 2024, 47% lower than $256 million in 2023, but an 8% uptick from $125 million in 2022. Funding into Internet-First Insurance Platforms was $51.7 million in 2024, down 78% from $236 million in 2023, and a 56% decrease from $115 million in 2022. The Employer Insurance segment raised $6.5 million in 2024, a drop of 65% from $18.5 million in 2023, and a growth of 27% from $5 million in 2022.

Notably, no unicorns emerged in the SEA InsurTech sector in 2024, mirroring the trend from 2023.

Acquisition activity in the SEA InsurTech sector also slowed, with only one acquisition recorded in 2024—down from five in 2023 and two in 2022. Roojai acquired Lifepal, an insurance comparison platform, marking the sector’s only acquisition in 2024.

Singapore continues to lead the funding ecosystem with $135 million raised in 2024, followed by Jakarta ($50.5 million) and Kuala Lumpur ($1.2 million).

Key investors shaping the SEA InsurTech sector in 2024 include Wavemaker Partners, East Ventures, and Openspace Ventures, who are the all-time most active investors. Y Combinator, Bee Next, Appworks took the lead in seed-stage investments in 2024, while EDBI, Peak XV Partners, KB Investment were the top early-stage investors.

Despite a sharp downturn in InsurTech funding, Southeast Asia’s resilience, evolving economic landscape, and growing government support provide optimism for future growth. The region’s ability to attract major global corporations and maintain its standing as a burgeoning tech hub underscores its potential to boost growth in the region.