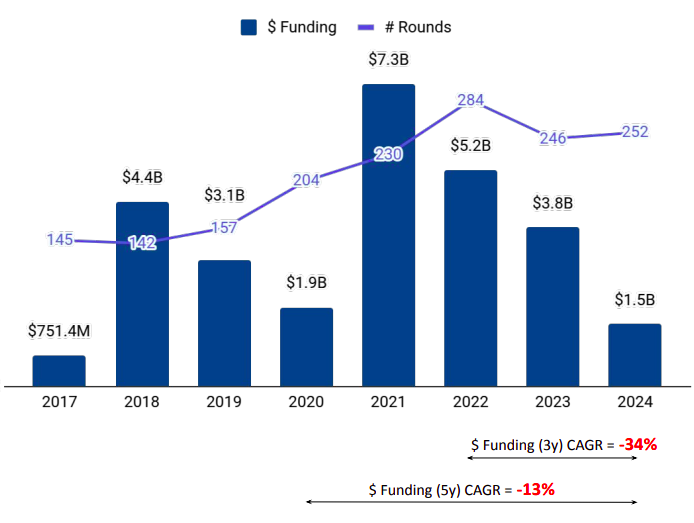

The South Korean tech startup ecosystem has faced a sharp downturn in 2024, recording its lowest funding levels in seven years. After peaking in 2021, the region has experienced a continuous decline in funding. The decline can be attributed to a combination of political instability and economic challenges. Additionally, the South Korean Won has weakened significantly, dampening consumer confidence and slowing job growth. The ongoing funding winter has also shifted investor focus towards late-stage firms with proven business models, further limiting access to capital for early-stage startups.

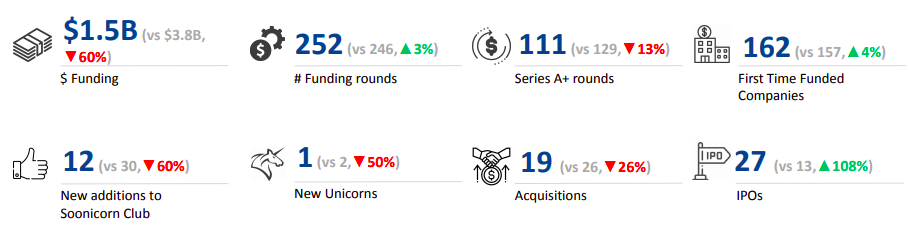

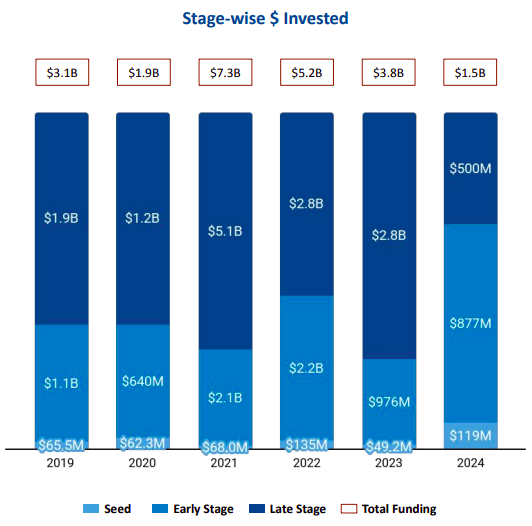

In 2024, The South Korean tech startup ecosystem witnessed total equity funding of $1.5 billion, down 60% from $3.8 billion in 2023. This is also a 71% decline from the $5.2 billion raised in 2022. Seed-stage funding rose 142% year-over-year, reaching $119 million in 2024, compared with $49.2 million in 2023. Early-stage funding stood at $877 million, a 10% decrease from 2023 and a 60% decline from 2022. Late-stage funding was the most impacted, plummeting 82% to just $500 million from $2.8 billion in both 2023 and 2022.

A significant decline was observed in the number of mega-rounds, with only one $100 million+ funding round in 2024, as against nine in 2023. Rebellions reported the largest funding round of the year in this sector, raising $124 million in its Series B round. The company secured a total of $138.4 million across two funding rounds in 2024.

Enterprise Applications, Semiconductors, and HealthTech were the top-funded segments in 2024. The Enterprise Applications sector led the funding charts with $568 million in total capital, marking a 40% increase from $405 million in 2023. Semiconductor companies witnessed an impressive 171% growth, raising $271 million in 2024 compared to $100 million in 2023. Rebellions accounted for 51% of the total funding in the semiconductor sector. HealthTech startups secured funding worth $177 million in 2024, a 36% rise from $130 million in 2023.

The IPO landscape witnessed a sharp upward move, with 27 companies going public in 2024, more than double the 13 IPOs in 2023. Finemedix was among the notable public listings in December 2024.

However, the number of acquisitions lowered to 19 recorded in 2024 from 26 in the previous year and 34 in 2022. TSC’s acquisition of Bluebird, a provider of enterprise mobility solutions, was one of the notable deals in 2024.

ABLY, a South Korean e-commerce platform for personalized style shopping, was the only new unicorn of 2024. The company raised $71 million in its Series B round, achieving a valuation of $2.1 billion.

&zN8wj;

Seoul continues to dominate South Korea’s tech funding landscape, securing 71% of the total funds raised in 2024. It remains the top-funded city, followed by Seongnam-si and Yongin-si.

Korea Investment Holdings, IMM Investment, and Aju IB Investment were the most active overall all-time investors. FuturePlay, Mashup Ventures, and STH emerged as the leading seed-stage investors in 2024, while Hana Ventures, Shinhan Venture Investment and Atinum Investment were the top early-stage investors. DS Investment Partners, Jeneration and RPS Ventures were the most active late-stage investors in 2024.

While 2024 has been a challenging year for the South Korean tech ecosystem, there are signs of potential recovery. The government’s push for revitalization, combined with the country’s strong technological capabilities and skilled workforce, may set the stage for a rebound in the coming years.