Tracxn, a leading global SaaS-based market intelligence platform, has released its Geo Quarterly Report: US FinTech Q3 2024. The report, based on Tracxn’s extensive database, provides insights into the US FinTech space.

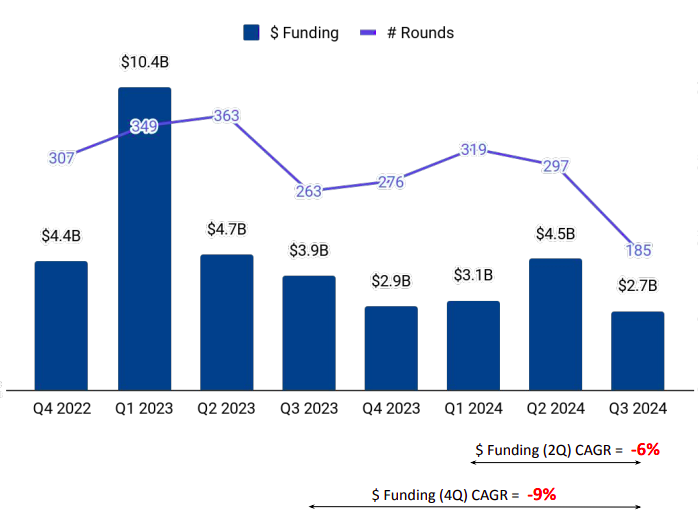

The US boasts of a bustling FinTech landscape, with more than 7K funded companies and 137 active FinTech Unicorns. Though the US ranks first globally in terms of funding in the FinTech sector in Q3 2024, this is the least funded quarter in the past five years. Q4 2021 was the highest funded quarter in this space, after which the funding started to experience a steady decline.

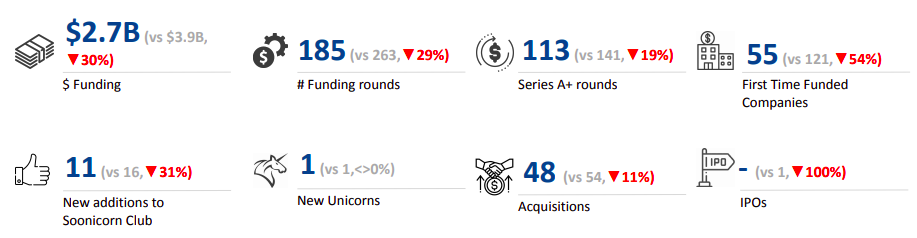

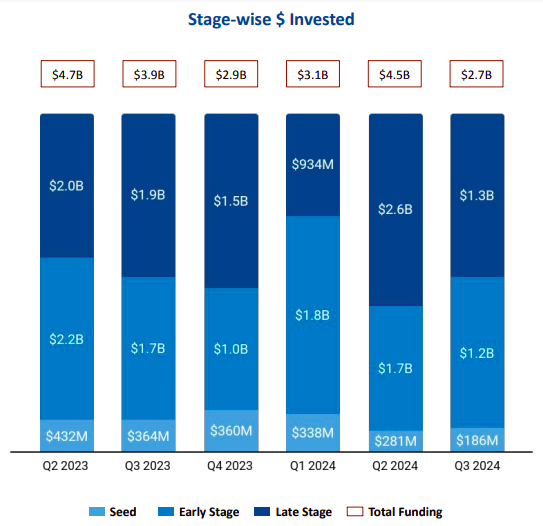

The US FinTech startup ecosystem raised $2.7 billion in Q3 2024, a 30% decline compared with $3.9 billion raised in Q3 2023 and a 40% decline from $4.5 billion in Q2 2024. Late-stage funding in Q3 2024 fell 32% to $1.3 billion, from $1.9 billion raised in Q3 2023. Early-stage investments stood at $1.2 billion in Q3 2024, a drop of 29% from $1.7 billion in Q3 2023. Seed-stage funding, too, fell 49% to $186 million from $364 million in Q3 2023.

Three companies attracted funding of $200 million and above. Human Interest raised $267 million in a Series D round at a post-money valuation of $1.33 billion, while FLYR raised $225 million in a Series D round. Earned Wealth secured $200 million in a Series B round. Three other companies reported $100M+ rounds, with Aven becoming the only new unicorn in the third quarter of this year, after raising $142 million at a valuation of $1 billion.

Finance and Accounting Tech, Payments and Investment Tech were the top-performing sectors based on funding in Q3 2024 in this space. The Finance & Accounting Tech segment witnessed total funding of $643 million in Q3 2024, a drop of 34% compared to $967 million raised in Q3 2023.

Funding raised by the Payments sector fell 22% to $573 million in Q3 2024 from $737 million in Q3 2023. Investment Tech companies raised a total funding of $547 million in Q3 2024, 18% lower than the $669 million raised in Q3 2023.N8

The third quarter of 2024 was weak in terms of exits. None of the companies from the US FinTech sector went public in Q3 2024, as against one IPO each in Q3 2023 and Q2 2024. The number of acquisitions too, fell to 48 in Q3 2024 from 54 in Q3 2023 and 62 in Q2 2024. ShareFile was acquired by Progress at a price of $875 million, and Stronghold Digital Mining was acquired by Bitfarms for $175 million.

Among US cities, San Francisco and New York City together accounted for 50% of the total funding raised by the sector in the third quarter of this year. FinTech startups based in San Francisco raised $750.2 million, while those headquartered in New York City and Santa Monica raised $610.1 million and $225 million.

Y Combinator, Techstars and a16z are the overall top investors in this space. Y Combinator, Castle Island Ventures & Plug and Play Tech Center were the top seed-stage investors in Q3 2024, while Curql, Redpoint Ventures and Brewer Lane Ventures took the lead in early-stage investments.

The US government is taking several initiatives to stimulate investment and innovation in the FinTech sector, which could give a boost to these startups in the coming years.

(Data for Q3 2024 covers the period from July 1, 2024, to September 30, 2024)