Tracxn, a leading global SaaS-based market intelligence platform, has released its Geo Semi-Annual Report: Vietnam Tech H1 2024. The report, based on Tracxn’s extensive database, provides insights into the Vietnam Tech space.

Vietnam's tech startup ecosystem has navigated a challenging landscape in H1 2024, reflecting broader global economic trends. The latest data from Tracxn reveals significant funding reductions, yet certain sectors continue to demonstrate robust performance.

N8

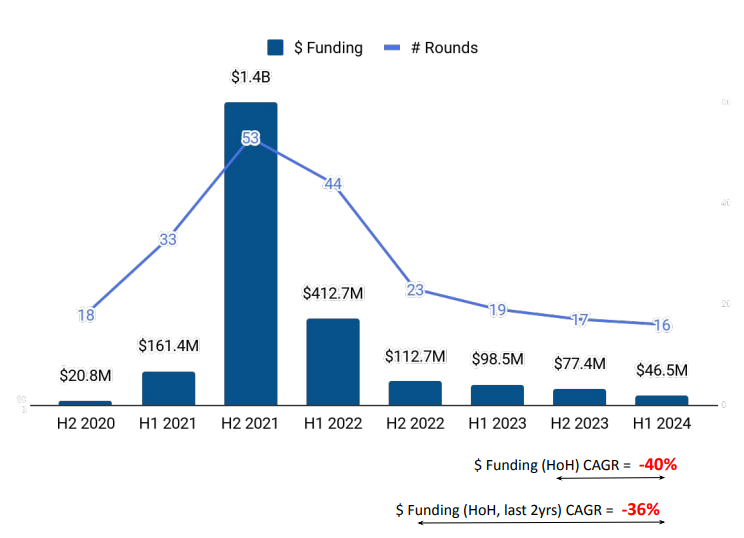

Ranking as the 45th highest funded country globally in H1 2024, Vietnam's tech startups raised a total of $46.5 million. This marks a 39.9% decline from the $77.4 million raised in H2 2023 and a 52.7% decrease from the $98.5 million raised in H1 2023, illustrating the shifting investment climate. In comparison, the United States, the United Kingdom, and China secured the top three positions for funding worldwide.

Vietnam tech startups garnered seed-stage funding worth $5.2 million in the first half of 2024, representing a 29% drop from $7.4 million in H2 2023 and a 23.5% decline from $6.8 million in H1 2023. Early-stage investments stood at $41.3 million, a 41% decrease from the $70 million raised in the latter half of 2023 and a 53.4% drop from $88.6 million in H1 2023. Furthermore, there was no funding for late-stage startups in H1 2024, mirroring the trend from H2 2023, whereas $3 million was raised in the first six months of 2023.

Ho Chi Minh City led the funding space, followed by Hanoi and Binh Thanh, showcasing the regional distribution of investment within Vietnam. Tech startups based in Ho Chi Minh City raised $36.3 million in H1 2024, while those based in Hanoi and Binh Thanh raised $7.7 million and $2.5 million respectively.

Sector-wise, Transportation & Logistics Tech, EdTech, and Retail emerged as the top-performing sectors in H1 2024, highlighting strategic growth areas despite the overall funding decline. Companies in the Transportation & Logistics Tech sector witnessed a huge spike of 940% in funding, from $3 million in H1 2023 to $31.2 million in the first six months of 2024. The Edtech segment, too, recorded a 280% surge in funding, from $2.5 million in H1 2023 to $9.52 million in H1 2024.

However, no new unicorns were created in H1 2024, continuing a similar trend in the previous period. The M&A landscape also saw a contraction, with only two acquisitions in H1 2024 compared to three in H1 2023. Notably, RHB Vietnam Securities was acquired by Public Bank for $15.2 million, marking the highest-valued acquisition in H1 2024, following the Home Credit Vietnam by SCBX.

Investment activity in Vietnam's tech ecosystem was driven by key players such as CyberAgent Capital, Insignia Ventures Partners, and Genesia Ventures, who remained the top investors overall. Northstar Ventures, Ansible Ventures, and Monk's Hill Ventures also stood out as significant contributors to the investment landscape in H1 2024.

Despite the funding challenges, Vietnam's tech startup ecosystem continues to exhibit resilience, driven by strong performances in key sectors and strategic regional investments.